Four Books That Will Make You Better At Managing Money

There is only one investment that can get you 100x returns and is totally risk-free. For a $10 price, they offer the best return on investment for your money. And they are Books. I have gained more useful knowledge reading them than from the traditional education system. So in this blog, I will list the best personal finance books I have read in recent years. I will explain to you the core concept of each book and why you should read it. If you are someone who wants to start investing and make some money or just be happy with the money you have, you have landed on the perfect page. So let's get started.

Rich Dad Poor Dad

The first book on the list is Rich Dad Poor Dad, written by Robert Kiyosaki. The book is written from Kiyosaki's perspective on how he was raised by two mentors or fatherly figures. One is his birth father, who was well educated, worked a day job, and earned a decent amount of money but never really got ahead financially. And the rich dad is the father of a friend who understood the rules of money, had his own business, and was a multi-millionaire. In the book, Kiyosaki compares the two strategies and explains how he made good financial decisions using advice from his rich dad.

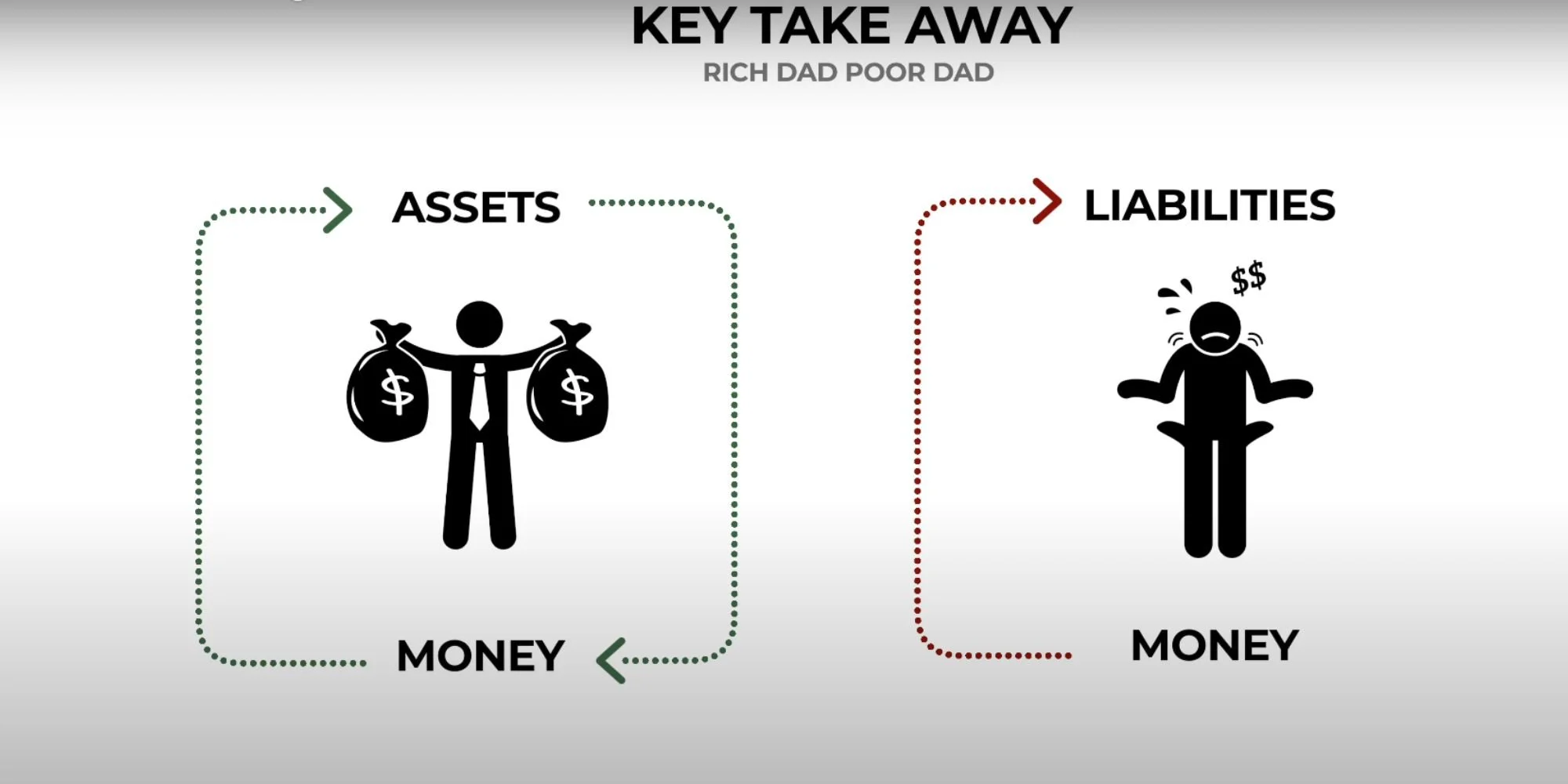

The key takeaway from the book is the difference between assets and liabilities.

Assets are anything that generates money and increases in value over time, like stocks, a business, or real estate. Anything that takes money out of your pocket is a liability, like the monthly payments on your car or your mortgage. Rich people buy more assets that generate revenue, and with that, they buy even more assets. But poor people use all their money to buy liabilities and become poorer. So, in a way, the rich make money work for them, and the poor and middle-class work for money.

I think this is by far the most important lesson from the book. You should take a moment and think about all the assets and liabilities in your own life. And try to tilt the balance more in favor of assets. Invest in the stock market, start a business, buy and rent out an apartment. Assets are what, that's really going to make you wealthy and enable you to leave the so-called rat race. Kiyosaki also takes a dig at the typical safe play attitude of the people.

“When it comes to money, most people want to play it safe and feel secure. So passion does not direct them. Fear does.”

He calls the traditional path of going to school, getting a job, working hard, and retiring an outdated mantra. Instead of working our entire life in somebody else's business and making other people rich, we should try to build our own. And for that, we need to improve our financial literacy and make better decisions. This is an excellent finance book for anyone who wants to build wealth, and it can force you to think outside the normal way. I will say, though, that the teachings are pretty high level. If you want really practical advice, I recommend the following two books on the list.

I Will Teach You To Be Rich

This book was written by Ramit Sethi, a self-taught expert in personal finance. This was one book that was recommended by many, but I kept away from reading it because somehow the title didn't connect with me well. Then I came across some of his interviews on YouTube and was totally impressed by the simplicity with which he presents his ideas.

In this book, Ramit manages to cut through the noise of conflicting and overly technical financial advice. The book has tons of practical advice, from using your credit cards to choosing the right bank and investment accounts to ultimately building a financial system that automatically grows your money.

And according to the author, the first step to getting there is taking responsibility for our financial life. Doesn't matter if you are a 24-year-old recent graduate who blows all of his fancy new salary on video games and takeout or a 35-year-old who sits on a pile of cash because he or she is afraid of losing the money.

We need not be an expert or be perfect at our finances to get rich. Just taking responsibility and getting started is more important than getting it right. And an excellent way to start is by automating our investments. We can do this by opening multiple saving accounts and moving money to them automatically. Whatever remains in the spending or current account, use it for our guilt-free spending.

The main reason I didn't save and invest much in the early days when I started earning an income was that I didn't like the idea of living frugally and sacrificing every happiness to have a better tomorrow. But Ramit has an alternative for that in his book. Think of all the things that bring you true happiness. It could be as expensive as a trip to the Maldives or as cheap as a morning cappuccino. Now spend lavishly on what you love and cut back mercilessly on those you don't. Just make sure that you don't get too overboard with the lavish spending part.

The book is written with American readers in mind, so there will be a lot of terms like 401K and IRAs. But if you can get past that, this book will definitely take you on the path to being rich. But everyone won't have time and effort to closely monitor their finances and manage their investments. Most of us need a simple, no-bullshit approach that can be easily executed. That's what you get from the next book on the list.

The Simple Path to Wealth

This book was written by J.L Collins, who is not yet a household name like Kiyosaki or Benjamin Graham in the field of personal finance. But if you start reading blogs among the early retirement community, you cannot help but learn about the man. Through his blogs and books, Collins offers a simple road map to building wealth and achieving financial independence. Spend less than you earn, invest the surplus, and avoid debt.

The book is more geared toward someone unfamiliar with investing and provides an easy-to-understand guide to choosing the right investment strategy and avoiding common mistakes. In the book, Collins stresses the importance of having a long-term perspective when it comes to investing. According to him, your goal should be to save up F_You Money.

This is the money that will help you to regain your freedom and would come around 25 times your annual expenses. And to get there, we must divide our financial journey into two stages. The Wealth Accumulation Stage comes while you are working, saving, and adding money to your investments. Collins asks us to keep it simple and allocate 100% of your investment portfolio to low-cost index funds such as Vanguard Total Stock Market Index Fund (VTSAX) or its ETF (VTI).

The Wealth Preservation Stage comes once your earned income slows or ends when you're closer to your retirement. At this stage, adjust 20-50% of your portfolio to include more safe investments such as bonds. The message throughout the book is straightforward. "Harness the world's most powerful wealth-building tool" – the stock market. It always goes up. Always. He compares the stock market to beer. When you pour a beer, you get both beer and foam.

Foam is all the temporary fluctuations in prices, the daily stock market reports, the expert financial advice, and below all that noise is the beer that truly matters. I love this analogy. For all of us average folks, we just have to ignore the noise and focus on the beer. The book is full of such metaphors along with parables and personal experiences. But the next book on the list is the one that made the most impact on my life. It takes a totally different approach to traditional financial advice and goes after the core reason why people behave the way they do with money.

The Psychology of Money

Let me tell you this. You won't get any stock recommendations or 100x strategies from this book. But this book will change how you look at investing and finances. The book explores the psychological side of money and how our finances are influenced mainly by our behavior more than any investment strategy.

“People from different generations, raised by different parents who earned different incomes and held different values in different parts of the world, learn very different lessons. And when that’s the case, a view about money that one group of people thinks is outrageous can make perfect sense to another.”

I know relatives in my family who prefer to keep most of their money in cash or gold and stay away from investing in the stock market. When they grew up, the stock market didn't do much. So it's natural that they think differently of the market as such and would stick to traditional investment options, even though it doesn’t make perfect financial sense. Another important point made in the book is how we care too much about people's opinions about us and how we overspend to match up to that opinion.

This is one reason why people never seem satisfied with what they earn. So they take risks without considering the trade-off. We must realize that there are more important things in life than money. Reputation is invaluable. Freedom and independence are invaluable. Family and friends are invaluable. And your best shot at keeping these things is knowing when it's time to stop taking risks.. I just love that. So before next time you run after that NFT that can go to the moon or that investment strategy that can give you 100 times return, remember these words.

The book also stress the differences between the rich and the wealthy. According to the author, it's not the same. Rich is a current income. If you earn in a million range currently, you are probably rich. You can easily say if someone is rich by their clothes or the car they drive. But wealth is hidden. It's the income not spent. The nice cars, that were not purchased. The diamonds, that were not bought and the first-class upgrade, that was declined.

So you can never be sure if someone is wealthy because you can't see it from the outside, and unfortunately, you can't look into their bank accounts.

There are so many such gems of valuable information in this book that I can't summarise here in this blog. I have made a separate video on these books, which you can check out here.

Those were the main books I have read that hugely impacted my financial life and I hope they do the same magic for you as well.

Disclaimer: The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. It is important to do your own analysis before making any investment.